As our article Enterprise Value Versus Equity Value – Determining The Final Value In Transactions outlines, the final price paid for the “Equity Value” of a company is often substantially different from the headline price or “Enterprise Value” initially agreed between the parties of a deal at the point the LOI is signed.

The fundamentals behind Equity Value adjustments and the mechanics of these can be understood easily enough – however, the application of these principles to a specific deal is often complex and subjective.

Despite the value often at stake, and the potential for complexity, there is no set of agreed upon rules or standards for determining Equity Value adjustments in deals.

Given the many contentious areas and the lack of consensus on the core matters, an acquirer’s opinion of the final deal price can be materially different from that of a seller. This can lead to prolonged negotiations between principals and advisers, therefore causing delays, increased costs, undesirable outcomes and even aborted deals on occasion.

The working capital mechanism of a deal is an easy way for value to be lost if it is not structured and negotiated properly. Approached correctly, an acquirer or seller can use this mechanism to improve their respective pricing positions and to protect against hostile value shifting.

The working capital mechanism can form a point of disagreement between the acquirer and seller.

As outlined in our previous article, a common assumption of an acquirer’s offer is that the Target will have a “normal level of working capital” at deal close. This assumption will result in an adjustment to Equity Value to the extent working capital at completion is not “normal.”

A “normal” level of working capital (typically, the average working capital that is required to generate the EBITDA that served as the basis of the Enterprise Value inferred in the acquirer’s offer, or, the working capital projected to exist at deal close) will be a point of negotiation – and perhaps disagreement – and is essentially an element of the overall purchase price.

The quantum defined as being “normal” is typically a fixed amount set out in the SPA as “target working capital.” Here, the seller will pay the acquirer if working capital at deal close is less than this target amount. The acquirer will pay the seller additional consideration to the extent working capital at deal close exceeds the target working capital.

This mechanism is typically included within a deal structure to prevent the seller from stripping this capital from the company at or prior to deal close to the point where the acquirer would need to inject additional capital to fund operations post-close (effectively increasing the purchase price).

If there is no working capital adjustment on a transaction, this could present the following two problems:

- The seller may be incentivized to “manage down” the working capital (for instance, delaying a supplier payment), thereby increasing the upward Equity Value adjustment for cash, with no off-setting downward working capital adjustment; or

- Deal close may occur at a high or low point in the working capital cycle. This could be attributed to working capital seasonality (depending on the nature of the Target’s operations) or due to the timing of payments and receipts around deal close. Again, this would result in a cash variation and adjustment, with no off-setting working capital adjustment, which could create an undesirable outcome for either the acquirer or Target.

Cash is a non-working capital item.

Defining Working Capital

Put simply, this represents a measure of a company’s efficiency and its short-term “financial health.” The working capital formula is:

Working Capital = Current Assets – Current Liabilities

A company’s working capital ratio (Current Assets/Current Liabilities) shows whether a company has enough short-term assets to cover its short-term debt. A ratio below 1 suggests negative capital. A ratio above 2 suggests that the company is not investing excess assets. A ratio between 1.2 and 2.0 is deemed to be sufficient by many financiers.

If a company’s current assets do not exceed its current liabilities it may face difficulty paying back creditors in the short term. A declining working capital ratio over a longer time period could be a warning sign warranting further analysis pre-deal (as part of the. M&A due diligence). For instance, a company’s revenue may be declining and, consequently, accounts receivables will be seen as decreasing.

Working capital can provide investors with an idea of a company’s operational efficiency. Cash that is unavailable in inventory or tied up as receivables cannot be used to pay off any of the company’s obligations.

Therefore, if a company is not operating efficiently (for instance, slow collection of receivables) this will be evidenced by an increase in working capital. This can be evidenced by comparison of working capital from one month to another, whereby slow collection of receivables may be indicative of an underlying problem in the company’s operations.

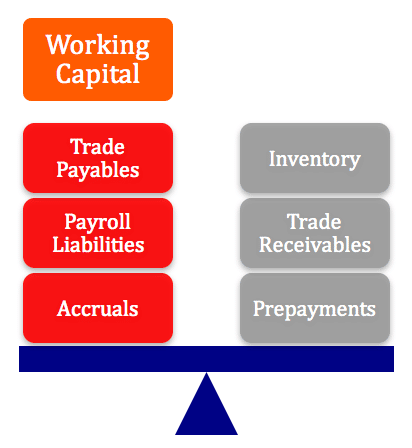

In the context of Equity Value adjustments, working capital does not have an agreed upon definition (furthermore, it is not defined within GAAP or IFRS). However, working capital is generally regarded as current operating assets (excluding cash) such as:

- Inventory;

- Trade receivables;

- Prepayments.

Less current operating liabilities are as follows:

- Trade creditors;

- Accruals;

- Payroll liabilities.

Any current operating assets or liabilities determined to be cash, cash-like, debt or debt-like should be excluded from working capital to avoid double counting (for the treatment of these items see Enterprise Value Versus Equity Value – Determining The Final Value In Transactions).

Defining a Normal Level of Working Capital (“Net Working Capital”)

Some companies may have a positive working capital cycle – for instance, debtors exceed creditors, while others may have negative working capital. Some may swing between the two.

Positive working capital is required to ensure that a company is able to continue its operations and that it has sufficient funds to satisfy both maturing short-term debt and upcoming operational expenses. Working capital may increase or decrease over time while some companies will experience significant swings in working capital due to seasonality.

The calculation of the normal level of working capital is a highly subjective area in the context of M&A.

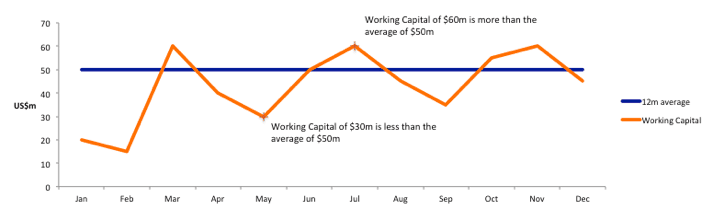

Typically, in considering what is “normal,” working capital will be measured over a certain period of time (the trailing 12 months leading up to deal close is often adopted) and an average taken. For companies subject to seasonality, it may be appropriate to use a reference period which fully averages-out monthly fluctuations (again, the trailing 12 months may be decided upon).

In the example above, using a $50m normal working capital target, if deal close takes place in May the working capital is lower than average (and therefore cash will be higher). The working capital adjustment therefore reduces the Equity Value by $20m (being the target of $50m less actual working capital of $30m), which supports the acquirer in funding the subsequent increase in working capital up to its average level of $50m.

In July, the position is reversed; the acquirer would pay an additional $10m for the excess working capital, which should be converted into cash over the following month(s) (via the payment of receivables, for instance). An acquirer should be aware that in instances where there are peaks and troughs in working capital over and above the observed average, short-term funding facilities might be required.

Agreeing on the Time Period

The period over which the normal or target working capital is calculated or pinned to may have a significant impact on the working capital number ultimately decided upon. In the instance of an expanding company (with positive working capital being the norm) an acquirer will prefer a more recent or future working capital reference period since it provides a higher target.

The working capital reference period is a contentious area of Equity Value adjustments. Compelling arguments can be made for various reference points, and this area requires careful consideration on each deal.

One possible approach is to align the working capital reference period to the EBITDA period underpinning the Enterprise Value (assuming the Target has been valued on this basis). The logic here is that the working capital target represents the requirements of the company at the level of earnings used for the headline price (being Enterprise Value).

Target working capital is often based on the average working capital of the company in the past twelve months. This period is often used because a full year average will remove any effects of seasonality. Secondly, the EBITDA number underpinning the acquirer’s offer is usually measured in the trailing twelve months leading up to deal close so it is practical for coterminous periods to be used.

Working capital can be driven by seasonality.

If a company is expanding quickly and an offer is based on forecast EBITDA, the target working capital should preferably be based on the forecast average working capital over the same period.

However, since forecast working capital is often not available, it is common to see acquirers apply the expected growth rate to EBITDA to historical working capital when calculating the working capital target.

In the instance of an expanding company, where future earnings have been forecast but historical working capital (where working capital is positive) has been used to set the target, this target will typically be lower than expected working capital in the future. This could result in the normal level of working capital factored into the deal price being artificially low, to the detriment of the acquirer.

It could be argued that if working capital at deal close exceeds the target and the acquirer pays an additional post-closing adjustment, then the acquirer is losing out. However, because the acquirer is receiving more working capital than expected (which can be used to generate earnings, which will convert to cash), there should be no change in the Equity Value paid at closing.

In addition to considering the reference period, normalization adjustments to working capital may need to be considered – for instance, one-off items have occurred over the reference period (which will distort the reported level of working capital). Since the monthly management accounts will not be audited, adjustments may also be required to present the monthly working capital in accordance with GAAP or IFRS.

How can Working Capital be Manipulated

An acquirer will always push for a higher working capital target, and a seller a lower target. One possible method to move the target away from the average is by making normalization adjustments for one time or non-recurring working capital items, or by excluding certain current assets or liabilities from working capital.

Working capital could also be manipulated by altering the way it is calculated under the SPA at deal close compared to how it may have been calculated historically (and in calculating the target). This could be achieved through judicious drafting and negotiation of the working capital definitions and related accounting principles in the SPA. Alternatively, it could be achieved when the acquirer is preparing the post-closing working capital statement.

The SPA will typically include specific policies in relation to the treatment of working capital.

For instance, the acquirer could adjust working capital amounts (while staying within the boundaries of the SPA) to come up with a lower closing working capital amount if the SPA includes wide and flexible accounting policies.

SPAs typically include that “working capital at deal close shall be prepared in accordance with GAAP” for the reason that GAAP is a widely understood convention. However, GAAP only provides guidelines, which are subject to interpretation.

As an example, with respect to “allowances for doubtful accounts,” GAAP outlines that a company should have a reserve for debts it does not anticipate collecting – yet GAAP does not set out how such a reserve should be calculated. An acquirer could argue that the reserve has historically not been adequate and therefore increase it on the closing balance sheet – thus reducing closing working capital and leading to a price adjustment in favor of the acquirer.

To prevent against such a tactic, a seller may propose very specific and detailed accounting policies in relation to the calculation of the closing statement (“completion accounts” in the UK). Rather than stating accounting policies should be “in accordance with GAAP” a seller could state accounting policies should be “consistent with past practices.” Indeed, a seller will often include a separate schedule of specific accounting policies to be used when preparing the SPA.

Ultimately, working capital mechanisms are often a problematic point of negotiation for the acquirer and the seller. However, a well-advised buyer or seller can take advantage of any such mechanism to support its desired price and to optimize any potential value shifts that may arise.