Few industries are undergoing shifts and transformation the way retail banking is today. An industry that, for decades, has struggled under the burden of regulation, complexity and legacy systems – appears poised to emerge. As technology increasingly becomes an enabler of better customer experience and more efficient operations, the sector is on the cusp of transformation. Transformation is not easy, however, and the growing pains are real. Banks are being stretched by the forcefulness and breadth of change – in addition to customer demands. Executive leadership must contend on multiple fronts. And the change is multi-faceted change too – evolving categorically with technology, customer service, demographic, behavioral and regulatory implications.

Accordingly, in the next 12-18 months, a number of business trends are expected to continue their emergence within the space. Four in particular, with broad industry relevance, are highlighted below.

1. Mobile Centricity & Digital Anchoring

Mobile banking is fast replacing the traditional bank-branch experience. While reorienting around this channel requires investment of resources and new sophistication, experience anchored in ‘digital’ will become a competitive differentiatorfor the most successful of banks. Much work remains, however, as banks and the existing workforce will need new skills to remain effective in the new digital era. It should be expected that the branch settings will remain, albeit functionally different. Leading retail banks will likely reduce physical footprints and focus the branch experience to be more educational and service-oriented, while moving transactional experiences to be more low-touch and digitally enabled. One example of this is Singapore’s DBS Bank, investing ~US$15 million to train its existing workforce in digital banking and emerging technologies, via an artificial intelligence (AI)-powered e-learning platform, curated curriculum, and module delivery.

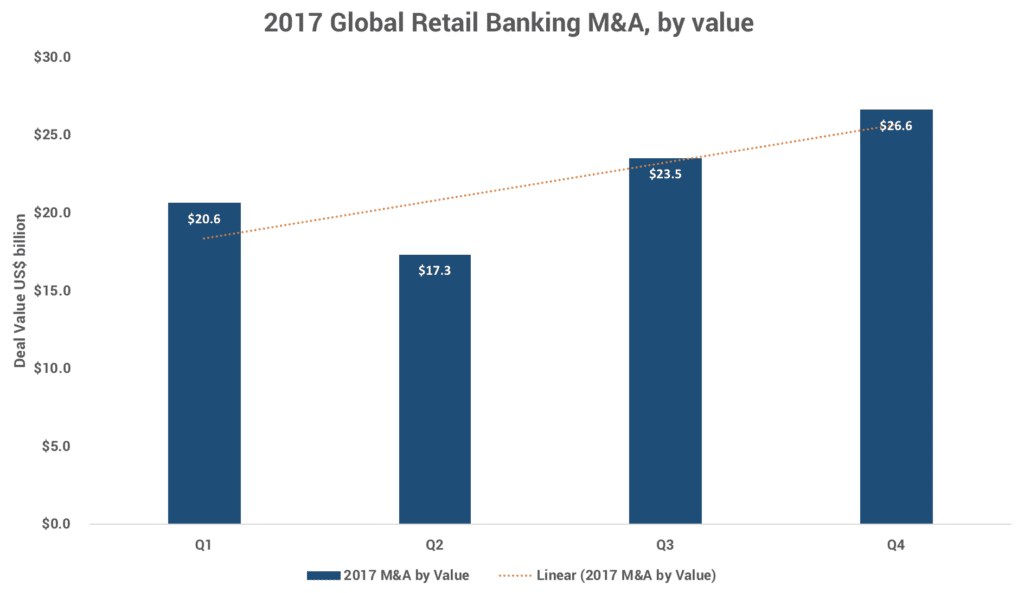

Above: 2017 Global Retail Banking M&A by deal value. Data: MergerMarket.

In a recent interview with Wharton Business School, Jay Sidhu, the founder of BankMobile, an all-digital consumer banking service noted, “[…] on an average, people walk into a bank branch once or twice a year. But they interact with their bank on mobile devices 20 to 30 times a month. From a business model perspective, bank branches are acquiring only 52 net checking accounts a year per branch.” Expanding on this, the implication (and solutions) will require that CIOs and technology leadership update internal systems, partner with sales, customer acquisition, marketing and service teams to deliver retail services in a digitally-accessible way. Internal system refreshes and external application and software assets for customer use will take the lion’s share of resources in the near term. Fortunately, emerging technology vendors, platforms and cloud offerings are set to support such a transition. From an M&A perspective, bolt-on acquisitions in these areas should be popular as a means to increase technology infrastructure and achieve back-office cost efficiencies. Bolt-on acquisitions are also likely to help banks fill gaps in their product offerings to customers.

2. Deeper Utilization of Machine Learning & A.I

American Banker recognizes how consumers have “…evolved from being wary of mobile banking to casually quizzing robots in their home about their spending habits.” Revolution in banking will continue in 2018 and beyond – and will increasingly be marked by future looking innovations that take advantage of technological advancements even beyond the new-normal of mobile and digital experience. One area of technological priority will be harnessing the informational advantage and service opportunity seen around artificial intelligence and machine learning.

Information is being generated by banking consumers and the institutions at a never-before-seen rate. PwC continues their discussion on technology’s influence in the space, noting: “leading players will harness both structured and unstructured information – from traditional sources (such as credit scores and customer surveys) and from non-traditional sources (such as social media, and cross-channel bank customer interaction data) […]. And they will collect and purchase other behavioral data (such as mobile location and purchase data) and […] develop advanced analytics capabilities to integrate this vast library of data, analyze it and create actionable insights.”

The explosion of data and emergence of tools to harness it means companies are able to deepen value and grow conversions with more tailored offerings. The industry should expect to see the continued growth of basic AI tools such as predictive banking and chat-bots. But to keep pace there will need to be richer incorporation of more advanced technology that is more predictive and personalized. Expect these cognitive technologies to move from beyond informational, to more transaction oriented.

3. Payments Modernization

Payment innovation has long been needed and is finally underway – a result of consumer desire and technological availability. In the U.S., the last significant improvement in payments ecosystem was the introduction of ACH (automated clearing houses) in the 1970s. But establishing emerging systems into the mainstream is difficult. The headwinds of the 2008 financial crisis, fraud and cyber-attacks, and regulation run into the promise of advancing technology, millennial expectations and increasingly global interactions. These converging pressures make standardizing new solutions a challenge.

Alternative digital players are gaining traction and will likely result in growing partnership or acquisition activity in the space. In this new reality, incumbents should also prepare for the inevitability of open architecture, such as open APIs, and how this will evolve the partnering ecosystem. Other advancements, such as peer-to-peer (P2P) payments (Venmo or Square’s Cash app, for example) suggest payment option variety is here to stay. Deloitte also writes how some players are eliminating intermediaries altogether with a horizontal digital payment solution (e.g., Amazon Pay).

This also reinforces the role mobile and smart devices will play in how consumers make payments. The customer will be able to select between account providers (e.g. credit providers, deposit accounts) or locally stored value. Acceptance will be universal (with common cross-network payment protocols) as installed services become mainstream and multi-currency capabilities will be the new normal. Customers will be able to make and receive payments based on any number of identifiers, such as email or phone number.

4. The Fintech Revolution

While fintechs have provided the competitive impetus to get incumbents to innovate, they’ve yet to take full control of the industry. The role of fintechs in the near future will remain one of providing solutions that are replicated or acquired by banking incumbents, and driving symbiotic partnerships in the space. Still today, legacy banks have market leadership due to three factors (i) regulatory barriers to entry (ii) the natural inertia of customers to switch; and (iii) the capital to absorb, partner with, or replicate fin-techs.

While fintechs may not overtake the industry, they have a crucial role to play in enabling creative digitization. Fintech-built companies have birthed ideas from blockchain and Ripple to robo-advisory services, and “one-click” banking. While they have not yet created the “killer app” to secure dominance, their niche technology and operating models are disruptive. Accordingly, banks are poised to look to fintechs as investment targets and partners, not just for financial return potential, but for the acquisition of IP to maintain relevant during industry upheaval and an eventual reorganization. This idea is termed “fintegration” and is probably the most apt term for how fintechs and legacy retail players will co-exist in the future.

Implications for Banking M&A

As expected in a period when innovation is readily embraced, M&A activity is set to increase. In pursuit of new advantage, competitive shifts, reinvention, organizational agility and information advantages, banks will look externally for investment and partnership solutions to establish leadership in their respective ecosystems.

Yes, 2018 may be the year that banking-related M&A really starts to take off.

As Deloitte’s annual outlook suggests, favorable policy developments and clarity on US tax reform may provide some catalyzing affect around deal making. It is expected that M&A activity will center around these themes: gap-filling to bolster legacy technology and back-office improvements, fintech plays to improve digital customer experiences and address blockchain and other disintermediation trends and lender consolidation with the expected interest rate environment.

Of course, M&A in the banking sector comes with its own set of unique challenges. Beyond the integration complexities involved in institutional mergers of any kind, banking and finance must often contend with strict federal regulatory or compliance mandates, branch networks, customer segments with sensitive data and other fragilities.

Operational efforts in this space should center around Governance & Structure, Digital M&A Tools, Preparation, Execution & Results Tracking.

Governance & Structure

M&A integration teams need to enjoy dedicated structures (i.e. – available resources, centralized control, multi-functional group involvement) and a comprehensive view of objectives, target outcomes and decision-making autonomy.

This guidance and leadership clarity will empower integration teams and keep efforts from being derailed because of unclear outcomes, or by unintentionally creating process ‘monitors’, as opposed to process managers or leaders. Failure here often looks like assigning insufficient or sub-optimal resources to the process, a lack of comprehensive dialogue at the executive level on outcomes or limited decision-making rights by key teams and participants.

Digital M&A Tools

In Deloitte’s 2018 Banking & Securities M&A Outlook, the following advice is offered with regards to running an efficient M&A process.

Before starting your M&A engine, it is important to remember—especially for those who have sat out deal-making in recent years—that the M&A process has evolved since the financial crisis. It now requires greater attention to detail in the depth and breadth of pre-signing due diligence and the front-end investment on synergy validation. Today, we are seeing savvy players leverage digital, analytic, and machine learning/cognitive tools to expedite post-deal integration and maximize value realization. Finally, potential sellers and buyers should make certain their playbook and deal processes are current to maximize the efficient expenditure of time and resources. And because both boards and regulators have a larger seat at the table at deal onset, it is prudent to communicate regularly with both constituencies throughout the deal process.

See here for how Midaxo can support your Digital M&A process.

Preparation

Preparation means having both broad, high-level milestones defined as well as business unit level and functional activities mapped. This is a multi-disciplinary stage requiring central project leadership and support service participation from IT, human resources, communications and marketing, for example. Teams need to be working toward target outcomes and have detailed plans – with risk-mitigating components in place – that capture inter-dependencies and provide the go-to strategy roadmap to be deployed when the deal closes.

Execution & Results Tracking

At the center of the integration execution process is a deal team delivering centralized coordination and reporting. This team is working with functional business units and delivering on standard integration fronts such as: personnel management, external stakeholder communications, training, systems management, compliance, lending operations and other standard PMI activities. This team needs to be communicating frequently and in a relevant way to internal and external audiences.

This stage is supported when methodologies and plans are laid in advance. Tools and templates, such as a post-merger integration checklist and M&A analytics, can be a critical enabler of thorough and efficient deal execution and results tracking.

Takeaway

New participants and emerging industry trends are making the retail banking industry as dynamic as it’s ever been. Transformation is unpredictable, but one thing is certain: it will spur competitive movement and M&A will play a role in this.

It is easy to be overwhelmed by the scope of tactical activities required around financial service and banking M&A. In leveraging Midaxo’s suite of tools and M&A software, companies can help preserve deal value and improve the likelihood of a successful and a repeatable deal experience.