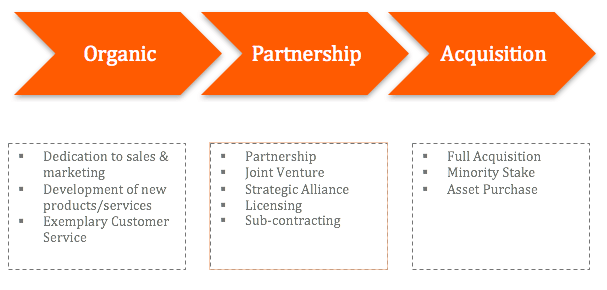

There are two main ways for a company to grow. One is via increasing sales and the general size of a company’s operations over time – a strategy often referred to as “organic” or “internal growth.” The other is via acquiring another company or a number of companies (it is also possible for a company to pursue growth via some form of coalition/partnership such as joint venture, licensing or strategic alliance).

Organic growth is typically associated with slow and steady growth achieved over a number of years (or decades) via a sustained dedication to sales, marketing and customer service.

Growth via M&A, conversely, can provide a company with the potential to grow significantly overnight, to fill a portfolio gap, or the opportunity to boost long-run competitive advantage via the unlocking synergies and economies of scale. Growth via M&A can also position a company more favorably when it comes to future exit options (typically, a large company with diversified revenue and customer channels will be more attractive to a prospective acquirer).

Growth via acquisition can offer a company the potential to grow significantly overnight.

Arguably the greatest benefit of pursuing a growth strategy via M&A is the rate at which it can enable growth. For instance, if a company with revenue of $10m a year acquires a target with with $10m of revenue, the acquirer can effectively double its size (in revenue terms at least) overnight.

Additionally, an acquisition may provide the opportunity for the acquirer to rapidly enter new markets and target new customer segments (including international) via utilizing channels the target already has in place.

An acquirer could specifically choose to expand their geographic footprint into new states or countries, by seeking to acquire a target based outside of their immediate geographic area. Alternatively, if the acquirer markets their products/services to a limited number of customers it might be able to access or attract new customers via a “horizontal acquisition” – whereby a target with operations similar to the acquirer’s is acquired (often a competitor).

Growth via acquisition can provide access to new geographies and customers.

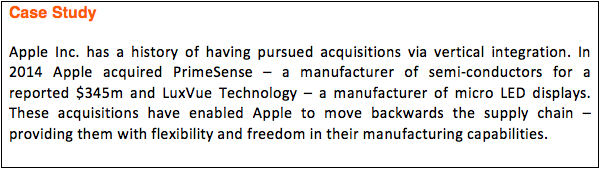

An acquirer may also consider making a vertical acquisition – the acquisition of a target sitting somewhere along the acquirer’s supply chain. For instance, a manufacturer may acquire a supplier of key components earlier in the supply chain so as to reduce costs and safeguard the supply of essential raw materials. Vertical integration can be achieved in two ways:

- (i) “backward integration” – an acquirer growing backwards along the supply chain, such as via acquiring a supplier of raw materials/key components, and

- (ii) “forward integration” – an acquirer growing forwards along the supply chain – such as via acquiring distribution channel selling to the ultimate customer.

Acquiring or merging with another company is often an expensive and time-consuming undertaking, requiring significant financial and people resources to cover the potentially extensive M&A due diligence, deal closing and post-merger integration (PMI).

Smaller companies will often lack the financial resources to undertake an acquisition in cash. In such an instance, an acquisition will typically have to be financed (at least in part) via debt or equity. An equity-funded acquisition (share-for-share exchange) will result in dilution of the acquiring shareholders, and potentially, a loss of control. Introducing debt will mean that the monthly servicing of debt (and likely, banking covenants) will need to be considered.

When analyzing the potential cost of an acquisition, an acquiring company should carry out a detailed appraisal comparing the cost of the acquisition and anticipated return on investment (ROI) with the costs that would be incurred to achieve the same growth organically.

Costs associated with organic expansion typically include sales and marketing, human resources, R&D and product development costs. Additionally, the amount of time it would take to achieve growth organically (rather than via acquisition) should be considered.

Key Considerations Pre-Acquisition

- Does growth via acquisition offer the best route for the acquiring company or should growth be achieved organically?;

- What is the target company’s potential for success?;

- What challenges will be faced and what changes will have to be made to the target company?

- How extensive will any necessary changes be and how necessary are they for the full potential of the target to be realized?

- To what extent will the target be integrated with the acquiring company?;

- Will the target generate sufficient earnings to pay for itself and provide a suitable ROI over a reasonable time frame?

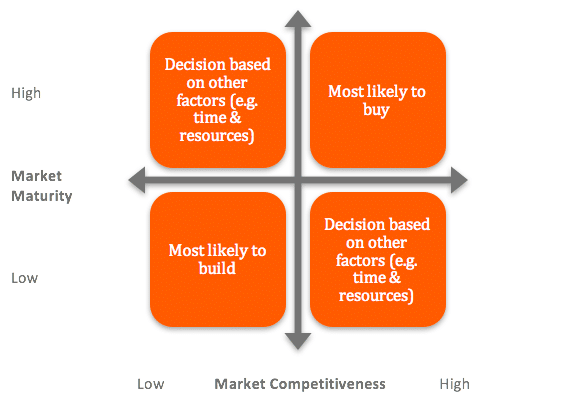

To Buy or Not to Buy: Key Decision Factors

Market maturity and competitiveness are key contributing factors when it comes to appraising whether to buy or build.

If a company is looking to enter a mature and competitive market for the first time (perhaps as part of a diversification strategy) buying is likely to offer the best route to market. If a company is looking to enter a new market where competition is relatively low, it is most likely to build. However, both the aforementioned strategies are dependent on a company being able to deploy sufficient resources to a buy or build strategy (time, cash, people, etc.).

Where the market is new but competition high, or where the market is mature but competition low, a company will need to appraise whether buying or building is most appropriate. As part of this strategic appraisal, factors such as time to market (e.g. building a new software platform versus buying one) and resources (cash and people) will be key.

A key advantage of pursuing an M&A strategy to achieve growth is the opportunity for synergies between the acquirer and the target to be realized. Synergies may include greater efficiency, lower overheads (achieved through the sharing of internal resources) and general economies of scale.

One significant drawback of growth via acquisition is the merging of two potentially very distinct corporate cultures. M&A deals can add up strategically and financially but not culturally. While it is easy for a deal to be treated as a financial transaction and to quantify the synergies, it is more difficult to predict how the combining of two corporate cultures (often very distinct and sometimes built up over many years) will succeed.

Indeed, merely considering growth in terms of revenue or profits is not enough. Rather, a company considering growth via acquisition should adopt a holistic approach, in which culture and people issues are key considerations. Therefore, it is critical to consider culture and people as part of the due diligence before proceeding with an acquisition.

How Many Targets to Funnel?

How many targets need to be considered in the M&A pipeline before a deal can be closed? This will depend on a number of factors, including the respective industry sectors of the acquirer and targets, the quality of the targets and the number available, previous sector consolidation, readiness of the targets to enter into an M&A process and the readiness and sophistication of the acquirer.

A buy-side “M&A funnel” may process in excess of 100 appropriate targets – however, only a few prospective targets will end up in the mix and subject to a due diligence process. It is notable that targets considered as “off-market” (i.e. not actively marketing themselves for sale) are commonly far less prepared for a buyer to make an initial approach. Accordingly, in such instances, acquirers must carry out more preliminary research when no sell-side representation is in place.

It might be necessary to add 100s of potential targets to the “M&A Funnel” before a suitable fit can be found.

It may be necessary for an acquirer to work through 100s of potential targets (many of which may have no desire to be acquired) as a part of M&A pipeline management and to eliminate a significant number of these at the outset (where they do not meet the relevant investment criteria).

After conducting this initial screening process, an acquirer may undertake additional research on the targets, further eliminating a large number of potential targets. After a suitable level of research, typically involving a very detailed due diligence checklist, has been undertaken, the acquirer may appoint a buy-side investment banker to schedule initial meetings and discussions with half or less of those that meet all the desired criteria (this may be done in unison with an internal business development representative).

Once the targets have been further refined (and the funnel narrowed) a small number (sometimes none) will make it to receiving a Letter of Intent (LOI).

Ultimately, if a target meets an acquirer’s desired investment criteria, the chance of connecting with a target that is willing to discuss a potential deal is low. Therefore, a wide targeting process is required to identify all available targets and to maximize the chance of one actually making it to the deal stage.

Why Expand via Acquisition?

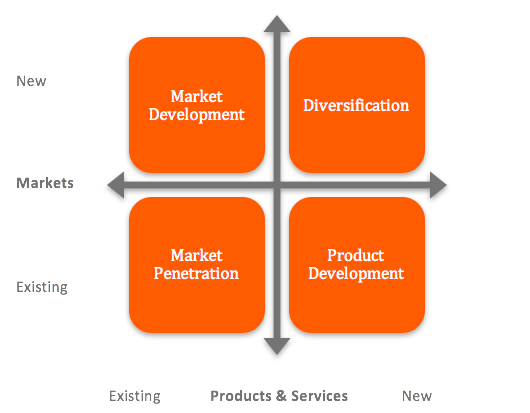

Acquisitions are often justified on the basis of a number of broad/vague strategies – including buy-and-build, roll-ups or consolidation. While these strategies can create value, they often fail to do so. Rather, an acquisition’s strategic justification should be a specific expression of the acquirer’s strategy and not an ambiguous concept merely labeled as “growth.”

Above: The Ansoff Matrix might be a bit “Strategy 101” but it is a useful tool in outlining the fundamental reasons as to why a company may pursue new or existing markets and new or existing products and services.

1) Improve the Performance of the Target

Seeking an improvement in the performance of a target is one of the most commonly cited value-creating acquisition strategies. Here, an acquirer can buy a company and significantly reduce operating costs to improve margins and cash flow. In some instances, the acquirer may seek to fast-track revenue growth.

This is a strategy often adopted by private equity firms (especially those focused on “turnaround” opportunities). It is easier to improve the performance of a company with low margins and low returns on invested capital (ROIC) than that of a high-margin, high-ROIC company – therefore, preference may be given to such companies.

2) Remove Excess Capacity via Consolidation

Mature industry sectors can often develop excess capacity. For instance, established companies may look for ways to squeeze more out of the production process, while new competitors continue to enter the industry. A combination of higher production from existing capacity and additional capacity from new entrants generates a situation where supply exceeds demand. However, companies are often reluctant to shut down production facilities to reduce excess capacity (unless an acquisition has been made and closure would not result in a smaller company).

Consolidation could also arise from a number of companies divesting of some of their product portfolios or research and development projects, for instance. While there is considerable value to be generated from removing excess capacity via consolidation, most of the value will fall to the seller’s shareholders, not the acquirer’s.

3) Fast-Track Market Access

Small companies with innovative/niche products often encounter difficulty in reaching markets for their products. Small software companies, for instance, may lack the large sales forces required to generate relationships with the many users they require. Larger software companies may acquire smaller companies and utilize their large-scale sales teams to fast-track the sales of the smaller companies’ products.

IBM previously pursued such a strategy in its software divisions. Between 2002-2009, IBM acquired around 70 companies for approximately $14b. By channeling the products of the target companies through a large-scale, global sales team, IBM estimates its revenue increased by 50% in the first two years following each acquisition and by an average of more than 10% in the following three years.

4) Acquire Skills or Technologies Faster & at Lower Cost

Growth via acquisition can allow a buyer to acquire skills (people skills or research and development capabilities) or innovative technology more quickly and at a lower cost than if this were to be developed in-house. Essentially, an acquisition in this context can solve critical time-to-market issues.

Between 2006-2014 Google’s acquisition strategy was driven by a desire to acquire key talent. Indeed, an article by Time Magazine suggests, “when a firm is making a tech acquisition, they’re buying the talent as much as they’re buying the technology.”

Furthermore, Jon Sakoda of US venture capital firm New Enterprise Associates, in speaking about Google, asserts, “first and foremost, their acquisition strategy has always been about talent. If you look at the vast majority of the acquisitions that they make—they are acquiring great people and frequently are acquiring people with domain expertise.”

5) Be a First Mover & Nurture Early-Stage Companies

Some companies may adopt a “first mover” strategy and seek to make acquisitions early in the life-cycle of a new industry or product line, before competitors recognize the potential for growth. Such a strategy necessitates a disciplined approach. The acquirer must be willing to make early-stage (often risky) investments, prior to competitors and the rest-of-the-market realizing the industry’s or target’s potential (this can often involve the acquirer taking a gamble on new or emerging technology).

An acquirer pursuing such a strategy will need to make “multiple bets” and should expect that many investments of this nature will fail. Furthermore, an acquirer will need to possess the relevant skills and expertise to nurture the target so as to realize its full-potential. This type of acquisition is often referred to as a “tuck-in” or “bolt-on” acquisition – where the acquired company will be bolted-on or tucked-in to a division of the acquirer.

6) Roll-Up Strategy (As Part of a Buy-and-Build)

A roll-up strategy entails the consolidation of highly fragmented markets, where the competitors are too small to achieve economies of scale. This strategy is best adopted when an acquirer as a group can realize considerable cost savings or achieve higher revenues than individual companies can. Size (or the potential size of the organization resulting from a roll-up) is often not the driving force behind this strategy.

Rather, a successful roll-up may be achieved where the acquirer targets acquiring multiple locations across many cities so that cost savings can be realized. In the instance of an acquirer in the freight/cargo industry, for example, cost saving could be achieved via the sharing of vehicles and storage depots – which would be possible if multiple competitors were acquired.

Key drivers of a roll up/buy-and-build strategy may include:

- Economies of scale – the acquiring company or the target company may have access to more efficient sales and purchasing channels. Alternatively, the merging of two or more companies may facilitate new access to economies of scale;

- Capacity utilization – this includes the ability to centralize sales, manufacturing processes or R&D activities, for instance;

- Exit strategy – the creation of a larger organization achieved via a buy-and-build strategy opens up exit opportunities to larger investors (financial and strategic) that lack the resources/appetite for smaller transactions.

7) Improve Competitive Behavior via Consolidation

Some companies in highly competitive industries believe that consolidation will lead competitors to focus less on price competition and more on improving the efficiency of the industry. However, it is likely that unless an industry is consolidated to a limited number of companies (four to six), which can prevent new market entrants, pricing behavior will not change.

For instance, smaller companies (or new market entrants) often have to gain market share via low prices. Therefore, in the instance of an industry where there are twenty companies, a high number of acquisitions must be made before competitive changes will occur.

8) Transformational Merger/Deal

Transformational mergers do not happen often. The two companies have to be aligned and the management teams must have the requisite skill to execute the strategy. The desire to transform one or both companies is the most cited reason for such a merger.

A transformational merger changes the nature and operations of a company. Examples include acquisition of new markets, channels or products, the sale or merger with another company, or other types of deals that are likely to have a long-term impact on the company. Such a deal involves significant operational integration – the outcome of which could define the success of the company.

Transformational mergers have increased in number as the global economy changes. In line with these changes, some companies look to alter the way they conduct their business operations, their business model or how they address the issue of scale in context to specific changes to the industry in which they operate.

A transformational merger may be advantageous when contrasted to a stand-alone acquisition or tuck-in for the reason that it can provide an organization with the opportunity to look beyond its core competencies and move with changing consumer demand and global dynamics. An example is seen in the changing operations of Amazon.

Amazon has built physical warehouses to cover different departments and utilizes advanced logistics and automation software to ensure products reach customers within the shortest time possible. As part of this strategy, Amazon acquired Kiva Systems (a robotics startup that services warehouses) in 2012 for a reported $775m.

Similarly, Walmart is targeting the fulfillment of online orders via making acquisitions of tech startups across social software, mobile apps, and cloud infrastructure.

9) Undervalued Target

Another way to create value from an acquisition is for the acquirer to “buy cheap” when a target is undervalued – with a view to increasing the value of the target via operational improvements (see point 1, above) or via integrating it with the existing operations of the acquirer.

Market sectors sometimes overreact to bad news stories, such as the failure of a single product in a portfolio with many strong ones – this could cause a target to be undervalued, for instance. While on paper an under-valued target may appear attractive, the costs of closing the deal and integrating the target into existing operations should be considered.

Furthermore, careful consideration should be given to whether the target supports the acquirer’s strategy and if it will actually provide a sufficient a return on investment – or rather, whether acquisition is being considered purely because of the under-value.

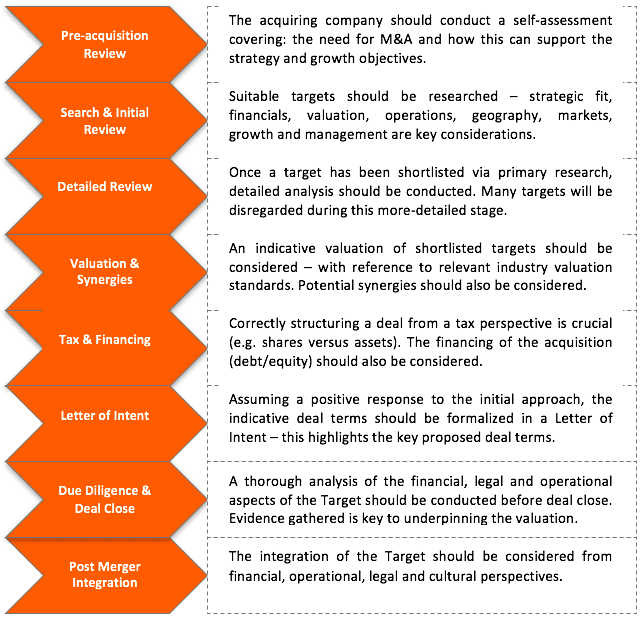

Stages of the Acquisition Process

Top 10 Acquisition Oversights

1) Chasing Deals At The Expense Of Business Operations

The acquisition process can be incredibly time-consuming. Many hours a week can be spent on profiling suitable targets, initiating discussions, agreeing deal terms, conducting due diligence and seeing the deal through to closing. It is therefore very easy for the upside factors associated with a deal to take priority over daily business operations.

2) Not Listening to Your Due Diligence

It is easy for “deal fever” to take over when so much time and energy has been put into a deal – often over a number of months, or more. However, the findings of the due diligence process must be considered – both the good and bad. In some instances, the best decision will be to walk away from a deal – the regret of doing so will be short-lived and another, more suitable opportunity will arise in due course.

3) Getting the Finding Structure Wrong

An acquirer may get the funding structure of a deal wrong – for instance, paying too much cash upfront or taking on too much debt. An acquirer may do this due to “deal fever” or because they overestimate the future performance of the acquiring company and the Target. While a seller may push for a greater percentage of the consideration to be paid in cash upfront, an acquirer should seek to secure an element of deferred payment terms – where some of the consideration is tied to the future performance of the Target (for instance, sales, EBITDA, retention of key management).

It is important that the acquirer does not “overgear” and commit to taking on too much debt – if the acquisition does not turn out as planned or the capturing of synergies takes longer than anticipated, this could make the servicing of debt difficult.

4) Ignoring the Softer Points of the Deal

The “softer” side of a deal should not be ignored. Those driving an organization’s M&A strategy may argue that a deal will bring about revenue increases and cost savings to the benefit of shareholders. However, it is the people within the organization, which, in the main, will contribute to delivering the increases in value.

On this basis the areas of communicating the deal in the first instance, considering the retention of key employees and the merging of cultures should not be ignored. For information on how to reduce organizational uncertainty and the “human side of M&A,” read more here.

5) Ignoring Integration

The First 100 Days post-deal are critical to ensuring successful integration and that the anticipated synergies between acquirer and target are captured. It is imperative that sufficient time is given to mapping out the First 100 Days post-deal – for more information on the importance of Post-Merger Integration and how to get it right see here.

6) Ignoring Difficult Decisions

Sometimes, an acquisition will not work for certain individuals. It could be that the change in culture brought about by an acquisition is too much for some people to comprehend and adjust to. In some instances, it may be better for some individuals to go their separate ways.

As the acquirer, coming to such a decision will not be easy – and having the conversation with the relevant individuals will be even more difficult. However, in the long run, making difficult decisions and acting on them can prove beneficial.

7) Failure to Delegate

For some owner-managers, delegation may not come naturally. Having developed a company from inception, an entrepreneurial-minded company owner-manager may feel uncomfortable delegating tasks or the running of the company to others, while they oversee an acquisition strategy. If an owner cannot “let go of the reins” they may need to consider if pursuing growth via acquisition is the right strategy for them.

8) Failing to Invest in the Right People

A growing company requires skilled individuals. Post-deal the focus may be on clearing debt as quickly as possible. However, if this comes at the expense of loosing key talent or bringing in new talent business operations may be impacted. Therefore, people should be considered as an asset and not as an obvious means of achieving cost savings.

9) Overestimating Synergies

On paper, synergies can appear attractive and may be one of the driving factors of a deal. However, synergies can often be overestimated and prove more difficult to capture than first thought. Therefore, potential synergies should be stress-tested in a financial model showing the debt servicing capacity of the company – this will emphasize the importance of not overestimating potential synergies.

10) Getting Carried Away

If a deal went well it may be tempting to pursue another acquisition soon after. However, before pursuing further acquisitions it is crucial that the First 100 Days have been considered and that the post-merger integration plan is on track. If the acquirer and target company are not aligned, or not working effectively, an element of re-adjustment will be necessary – further acquisitions should not detract from this.