As our recent article demonstrated an M&A strategy can help a company to expand, acquire new knowledge or technology, move into new geographical markets, or vastly increase output via one transaction. However, these benefits and opportunities often come at a significant cost to both the acquirer and target.

A typical M&A deal will involve lawyers, accountants/corporate finance advisers, investment banks and potentially, consultants. For the acquirer, in addition to these costs is the cost of the target company itself. In the absence of significant cash reserves, most companies will have to consider a range of financing options to acquisition funding.

There are a range of methods available for financing M&A activity. The most appropriate method will depend on factors including:

- The state of the acquiring company (size, reputation in the market, capacity to take on debt, credit rating, etc.);

- The type and magnitude of M&A activity being pursued (full acquisition or minority stake);

- The availability to leverage against company assets (such as unencumbered real estate);

- The availability of finance at the time of the transaction (for instance, following the 2008 “credit crisis” banks became more cautious in terms of their lending appetite).

Cash

Cash is arguably the most obvious and preferred way of acquisition funding:

- Cash transactions are instant and simple (for instance, cash does not require the same kind of complicated management as consideration via equity/shares would);

- The value of cash is less volatile than equity/shares and is not dependent on the performance of a company (which will be exposed to market volatility). However, if the transaction in question is cross-border exchange rates must be given due consideration. These can fluctuate significantly – most recently, as evidenced by the global market’s response to the Pound following the UK’s decision to leave the European Union. Additionally, currency exchange fees can add significant additional expenses to cross-border acquisitions;

- In the context of a cross-border deal, the price the acquirer pays for the Target may be subject to change up until the day of deal close if an exchange rate is not agreed upon/locked into earlier in the deal process.

While cash payment is the preferred method of acquisition funding, the price of M&A transactions can run into the millions or even billions – few companies have access to this level of cash reserves. However, there are ways of obtaining cash from other sources.

M&A transactions can run into the millions or billions – few companies have access to this level of cash reserves.

Debt

Borrowing can be expensive when undertaking an M&A transaction. Lenders (including shareholders of the Target who have agreed to accept deferred payments over an extended period) will require a reasonable interest rate.

Even if interest rates are low, in the context of a multi-million $ deal the costs of borrowing for acquisition funding can add up significantly. Interest rates are, therefore, an important consideration.

Low interest rates have fueled US M&A activity, for instance, with 2016 being a record year in terms of the total transaction value. In 2016, there were 17,369 recorded M&A deals in the US, with an aggregate transaction value of $3.2 trillion (Source: Reuters/MergerMarket).

A lower interest rate reduces the cost of borrowing and encourages investors to seek high-return opportunities. Conversely, an increase in rates increases the cost of borrowing and therefore, the value of deals, particularly if a significant portion of a deal is being funded via debt.

However, companies that have the benefit of significant cash reserves can sometimes be immune to rate increases (Source: KPMG: 2015 M&A Outlook Survey Report). Therefore, an acquirer with a strong balance sheet, demonstrable liquidity and with low/no debt may remain largely unaffected by a rate increase.

There are a range of options when it comes to acquisition funding via debt.

Term Loan/Acquisition Loan

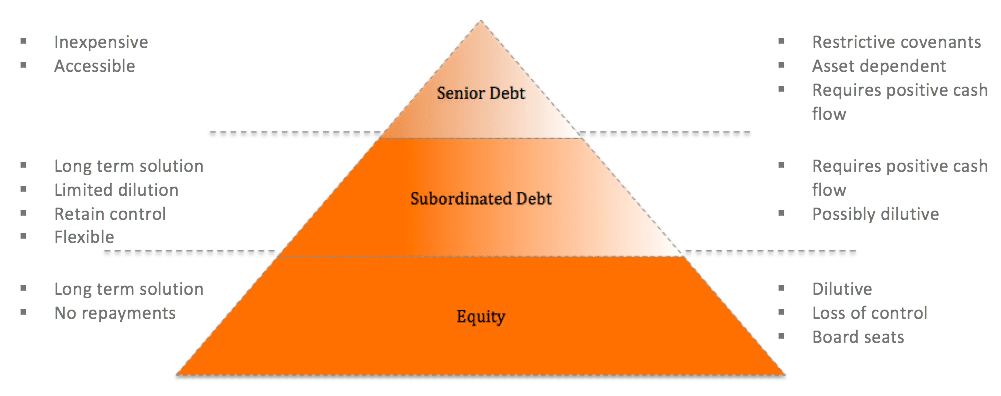

A term loan (or acquisition loan as it may be labeled) is a loan from a bank provided for a specific purpose, at a set amount, that is subject to a specified repayment schedule at a fixed or floating interest rate. A term loan will be provided by a “senior lender” – as is implied, this lender is ranked “senior” to all other lenders, meaning they would benefit from being paid before any other lenders in the event the borrowing company defaulted on payments, or was declared bankrupt.

Ranking under senior debt is “subordinated debt” – this is debt (or security) ranking below other loans and securities with regard to claims on a company’s assets or earnings. Subordinated debt may also be referred to as a “junior debt.” In the case of borrower default, creditors who own subordinated debt will not be paid until after the senior debt holders are paid in full.

The primary benefit of a term loan is that it can facilitate a large acquisition without the acquirer having to commit a significant level of capital or dilute their shareholding. If the acquisition creates a more profitable and valuable organization, shareholders will likely be of the opinion that taking on debt is worthwhile.

That said, if too much debt is taken on, or synergies are overestimated or not captured, the acquirer may not be able to service the debt and could face defaulting.

This high level of risk associated with taking on debt is the key reason why the share price of a publicly traded company usually falls when it announces news of an acquisition requiring debt. However, if investors believe the company will be able to pay down the debt, and increase the value of the shares, it could present a good opportunity to buy shares before they increase in value.

A term loan will typically collateralize by way of the Target’s own assets (such as real estate or plant and machinery). To secure a term loan, the acquirer must ensure the Target’s assets provide the adequate collateral for the loan required. Additionally, the acquirer should prepare financial forecasts of the combined entities to ensure they will generate sufficient cash flow to cover the principal and interest payments (maintaining positive cash flow could be challenging if the Target’s management team departs post-acquisition).

In terms of suitability, companies with few tangible assets are unlikely to be considered as suitable candidates for a term loan. Furthermore, companies that are only marginally profitable will be unlikely to be considered as suitable due to the greater risk of default.

A term loan may be sourced from one or a number of banks. Obtaining a term loan is often an expensive and complicated process. An investment bank, a law firm and accountants or corporate finance advisers are often required to correctly structure a term loan.

Term Loan – Advantages/Disadvantages

Leveraged Buyout (Including Private Equity)

A leveraged buyout (or LBO) entails the acquisition of a company using a significant amount of borrowed money to meet the cost of acquisition. The assets of the target company are typically used as collateral for the loans required (sometimes with the assets of the acquiring company). Similar to a term loan, a leveraged buyout allows a company to make an acquisition without having to commit a significant amount of capital.

Leveraged buyouts are often undertaken by private equity firms, and earned notoriety in the 1980s as a means of facilitating acquisitions. Arguably the main benefit of an LBO is that the company undertaking the acquisition (therefore, driving the LBO) only has to provide a low level of the financing (typically, around 80%-90% of the acquisition cost is financed through debt) yet it is able to make a large acquisition via significant leverage (this is distinct to a term loan – where leverage will not be as significant).

The underlying premise of an LBO is that the returns generated on the acquisition will greatly exceed the interest paid on the debt – therefore, providing a means of generating high returns while risking low levels of capital. The usual means for debt to be raised under an LBO is for the target’s assets to be provided as collateral for the debt (assets could comprise real estate, inventory, trade receivables, plant and machinery, etc.).

The high use of debt in an LBO (which is associated with a lower cost of capital than equity) reduces the overall cost of financing an acquisition. In turn, a reduced cost of financing provides the opportunity for greater returns to equity.

LBOs may take on various different forms – including management buyouts (MBOs), management buy-ins (MBIs) and secondary buyouts. A financial sponsor (typically a private equity firm) may be party to an LBO. Since a private equity firm can maximize its potential return by using high leverage (a debt to equity ratio) they have an incentive to deploy as much debt as possible when supporting an acquisition.

However, there is a danger of “over-leverage,” whereby a company does not generate sufficient cash flow to service the debt taken on as part of the LBO (this can lead to insolvency or settlement via a debt/equity swap, where the equity owners loses control of the company to the debt provider).

Under an LBO, the cash flow of the Target is used to service (pay interest) and pay down (payment of the principal) the debt. Therefore, while many companies may be suitable LBO candidates, those that generate significant cash flow are the most attractive (under a term loan the combined cash flow of the acquirer and the target, or sometimes just the acquirer, are used to fund repayments).

The returns of an LBO are determined by a number of factors including:

- Growth in the operating profit/cash flow of the Target (EBIT or EBITDA) prior to exit;

- The exit multiple on EBIT/EBITDA relative to the entry or acquisition multiple (multiple arbitrage);

- The amount of debt that can be paid off prior to exit (a high level of debt upon exit will reduce the Equity Value of the Target).

Real estate is one of many assets that can be leveraged against to provide funds to finance M&A activity.

Sale & Leaseback

While not strictly debt, in a sale-leaseback transaction, the owner of an asset (such as real estate) sells it to another party. The terms of the sale dictate that the seller will lease the asset from the buyer for a specified lease term (along with other terms and conditions negotiated by the parties). The former owner of the asset retains the use of the asset while receiving an up-front cash payment arising from the sale.

In an M&A process context, a sale-leaseback arrangement provides an immediate injection of cash into a company – therefore, providing the funds to support an acquisition.

Bridge Loan

A bridge loan is a short-term loan intended to “bridge” the gap between expected payments. A bridge loan could cover a partial cash shortfall experienced by an acquirer (typically, over a set period of weeks or months) and be paid off via the earnings generated by the Target.

Partially funding an acquisition via this means should be considered a last resort. Interest rates are typically higher than average, with late payment penalties being severe. Furthermore, utilizing a bridge loan to support an acquisition may raise concerns with the Target and other providers of finance (such as a bank providing a term loan).

Revolving Credit Facility/Lines Of Credit

A revolving credit facility or line of credit is a loan from a bank, often used to finance an acquisition. Distinct to a term loan, the borrower only pays interest on the amount of the facility it has used. For instance, a company may have a $10 million revolving facility, but if it has only used $4m to pay for an acquisition, the company will only pay interest on the $4m (and not the full $10m available).

A revolving credit facility can also be useful where a company has made an acquisition and requires short-term cash flow support. Interest rates will typically be higher than under a term loan but lower than a bridge loan.

Mezzanine Finance/Subordinated Debt/Convertible Debt

Mezzanine finance (sometimes referred to as “mezz”) is a type of subordinated debt, which usually has a convertible equity component (typically in the form of a call option, which gives the lender the right to purchase shares in the future, at a discount).

A lender, which is prepared to be subordinate to a senior lender, will typically require a higher rate of return (via a higher interest rate) – therefore making mezzanine finance an expensive option for acquisition funding. Mezzanine finance (or any derivative of this) is typically associated with companies considered to be high risk with the blend of debt and equity often creating complex deals.

Typically, in addition to issuing a loan (collateralized via the assets of the Target), a provider of mezzanine finance will take an equity position in the Target in which a larger percentage of equity can be obtained by converting the debt into equity (hence why mezzanine finance is labeled as “convertible debt”).

Rather than being the only source of acquisition funding, it may be most appropriate for mezzanine debt to be used in conjunction with other forms of debt (such as a senior term loan) and an equity element (via a private equity firm, for instance).

Corporate Bonds

The issuance of corporate bonds can provide a quick way for an acquiring company to raise cash – either from existing shareholders or members of the public. A company may issue a bond covering a defined period of time at a set interest rate. In buying bonds, investors are, in essence, loaning money to the company looking to make an acquisition, in the anticipation they will receive a return on their capital.

Once an investor purchases a bond their money is tied up and cannot be accessed until the maturation date of the bond. From the issuing company’s perspective, there must be the ability to pay the interest accruing on the bonds (this may be paid annually or bi-annually) so cash flow must be sufficiently positive. If bonds are issued to the public market the costs of issuance must be considered as this can represent an expensive means of raising acquisition funds.

In 2016, bond issuances reached a record high as companies took advantage of low interest rates in the US to fund their expansion plans and investors sought alternatives to cash savings. In 2016, more than $1.28 trillion of debt was raised via bonds – with $280 billion of this for M&A purposes (Source: Bloomberg & Reuters).

However, as with other forms of debt, the issuance of bonds, and investor appetite for them, is tied to borrowing costs. Bond issuances will therefore only represent an attractive means of financing an acquisition if they can be issued at a low cost while providing a suitably attractive return for investors.

Share-For-Share Exchange

This is arguably the most common means of acquisition funding. If one company is considering merging with or acquiring another, it is likely the acquiring company will have a healthy balance sheet and is in a strong position financially.

Under a typical share-exchange transaction, the acquirer will exchange shares (equity) in their company for shares in the Target. Financing an acquisition via this method is a comparatively “safe” option since the parties share risks between them post-deal.

Financing an acquisition via shares is also advantageous to an acquirer if their shares are overvalued on the market (in the instance of a publicly traded company) since more shares in the Target company will be received than if the transaction was being funded by other means (cash or debt). If shares are being exchanged where one (or both) companies are privately owned it will be necessary for independent valuations of the company/companies to be carried out so the respective share prices can be determined.

Under a merger, shareholders in both the acquiring and target companies can benefit in the long term, as they should receive an equal amount of stock in the newly formed company (the acquisition vehicle) that arises from the transaction (rather than receiving money for their shares).

The major drawback to using shares to fund an acquisition is volatility (there is always a risk that the share price of a company will fall, even if market sentiment for the company is strong at the time of deal close).

For instance, an unannounced or uncharacteristic acquisition could raise speculation in the financial press. Alternatively, global events outside of the control of a company can have an adverse impact on the share price, even if the company is performing well (the global financial crisis arising in 2008 and “Brexit” are two such examples of where significant value has been wiped off companies).

Even the most successful companies can be subject to stock market volatility.

Volatility made 2016 a bad year for stock-financed M&A transactions. For instance, in the first 26 trading sessions of 2016, the S&P 500 Index moved by 1% 16 times. In the first quarter of 2016, 77% of M&A transactions were funded with cash/debt (the highest level since 2013). Only one M&A deal over $1 billion was financed entirely by exchanging shares (Source: Financial Times).

It is difficult to predict what shares in a company may be be worth in the future – therefore, it can be understood why some companies may be reluctant to exchange shares rather than receive cash. In actuality, a compromise is often reached, where the acquisition includes a mixture of shares and cash. This reduces risk for both parties and allows both parties to preserve an equity stake in the new company.

Private Equity Investment

Small to mid-market companies are often family/privately owned and have significant amounts of equity available for distribution. All (or a proportion) of this equity can be sold to raise the funds required to support M&A. Those providing the funds are usually private equity firms.

Most private equity firms have specific investment criteria and stipulate which sectors/industries they will invest in (although some proclaim to be “sector agnostic”) and how much (sometimes referred to as the “cheque value”).

Furthermore, some firms will only invest if they can obtain a controlling equity stake and if their management is permitted to be actively involved in the day-to-day operations of the Target. Other firms may be passive and prepared to take a hands-off approach. Private equity firms typically invest for stretches of three to five years (referred to as the “investment horizon”) and will seek a significant return on their investment upon exit.

Initial Public Offering (IPO)

Initial public offerings (IPOs) can offer a good way for a company to raise money for a number of reasons (such as to allow existing shareholders a partial exit, or to fund extensive R&D activities) but in unison with M&A activity is one of the better times to carry out an IPO. The prospect of upcoming M&A activity can make investors optimistic about the future of the company. Planned M&A activity signals to the market that the company has ambitions to expand and a long-term strategy.

IPOs attract a lot of attention – therefore, timing an IPO in unison with M&A activity can help maximize investor buy-in and increase the share price. Indeed, existing shareholders could see the value of their shares increase significantly overnight. However, owing to the same volatility having reduced equity-financed M&A, IPOs can be an uncertain way of financing acquisitions.

The stock market can fluctuate as well as rise and newly floated companies are more vulnerable to volatility since they lack a track record to reassure investors. For this reason, IPOs are becoming less popular. 2016 was said to be a “dismal” year for US IPOs owing to the uncertainty surrounding the presidential election and a general gloomy economic outlook (Source: Reuters).

In 2016, US IPOs fell by more than a third from 2015. A quarter of the 102 companies that floated in 2016 were trading below their IPO price at the end of 2016. However, it is forecast that IPOs will increase in their numbers across 2017 as companies seek to raise funds and private equity firms seek to exit their investments (Source: Financial Times).

IPOs are set to increase across 2017 as companies seek to raise funds and private equity firms seek to exit their investments.

Takeaway

Where cash is not available, there are myriad ways in which M&A activities can be financed. The most suitable method will depend on factors such as the company – or companies – in question, the equity available, debt capacity, and the availability of assets. Each method of acquisition funding has its own risks, costs, and implications for the companies involved.