If you have decided to pursue an M&A strategy, and have identified a Target, consideration must be given to Due Diligence – an in-depth fact-finding exercise helping you to understand a Target in detail and establish whether the acquisition makes Strategic, Commercial and Financial sense for your organization.

M&A due diligence is a crucial stage in the deal life-cycle, where the Target makes available all financial, legal and other information that is material for the acquirer’s evaluation of the Target and its value. The process cannot be overlooked and can be viewed as an investigation into a Target prior to acquisition, investment, refinancing, restructuring, public listing (IPO) or similar transaction. Due diligence may require many months of dedicated time if the Target is large with a global presence.

The purpose of due diligence is to increase the acquirer’s understanding of key information supporting a transaction – for instance, what exactly is being purchased – therefore facilitating informed decisions while serving to identify and mitigate key risks pre-deal. During the due diligence process the Target is usually expected to disclose everything requested by the acquirer – unless the acquirer is a close competitor and the Target has a very strong position in negotiations.

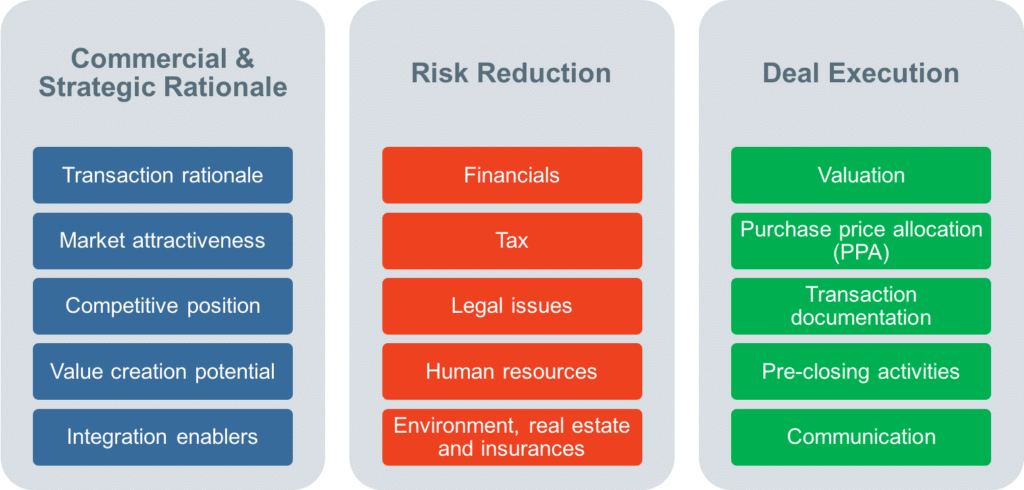

Companies conducting a high level of M&A activity often develop their own in-house M&A due diligence expertise, while those pursuing occasional transactions usually engage external advisors to assist them. A successful due diligence process should enable a potential acquirer be able to answer to any question from three conceptually distinctive areas – namely:

- Commercial & Strategic Rationale for the transaction;

- Risks Reduction (which may result in “deal breakers”);

- Deal Execution technicalities in order to close the transaction successfully.

Scoping a Due Diligence Engagement

The first stage of a due diligence engagement should be to consider the scope of the work required. In doing so, consideration must be given to the significance of the proposed transaction in the eyes of the acquirer, the size of the Target relative to the acquirer and the degree of access to information expected to be granted by the Target.

There is no prescribed format for what a due diligence engagement may encompass – rather, each engagement will be bespoke and tailored to the specific transaction and needs of the user. Having said that, companies that take on a high volume of deal activity typically catalog their considerations into a due diligence checklist that they can utilize on a recurring basis.

Financial Due Diligence

Financial due diligence covers a review of historic financial results including the balance sheet, profit & loss and cash flows of the Target (including any subsidiary companies to be acquired) with the possibility of particular attention being given to significant projects/contracts, the quality of earnings (contracted and recurring or one-off in nature), how realistic future financial projections are, the strength of the balance sheet (including the composition of assets and liabilities), the quality of management reporting and any tax issues arising – such as historic compliance with mandatory (corporate and social taxes) and any other specific taxes.

Commercial Due Diligence

Commercial due diligence includes a review of various commercial factors and should result in a detailed assessment of the Target’s positioning within its sector. Areas in scope may include market structure, size and conditions specific to the sector; sector-specific legislation (including that which may be implemented in the future); key competitor analysis, market share and positioning; barriers to entry; health of customer relationships/customer satisfaction and business plan achievability/limiting factors.

Operational Due Diligence

Operational due diligence gives attention to non-financial matters of a Target and highlights aspects of a transaction, which can foster improvements in productivity and profitability for the acquirer. These may encompass review and appraisal of systems and processes (including IT due diligence and the internal controls environment); review of the key management team and senior staff; staffing levels and other HR matters; insurances and risk assessment.

Legal Due Diligence

Legal due diligence is as important as financial and commercial due diligence in ensuring the success of a transaction and entails an investigation of any legal risks associated with the rights and obligations of the Target. Areas covered under the scope of an engagement typically include: Asset and property ownership; intellectual property (IP); loans; securities; employment; corporate governance; customer or supplier disputes and any pending litigation; incorporation, existence and ownership of the Target; existing contracts and adherence to regulations (including a history of any breaches).

Human Resources (HR) Due Diligence

HR due diligence should place most of its emphasis on a few critical areas: compliance with employment laws; employee contracts; employment related liabilities (such as redundancy payments and social taxes).

Environmental Due Diligence

Environmental due diligence is rarely the first consideration that springs to mind for acquirers, but liabilities can be substantial and difficult to uncover – thus presenting the possibility for an acquirer to be subject to unforeseen costs, which can be disproportionate to the overall transaction size in a worst-case scenario.

Pricing the Engagement

When using external advisors to perform due diligence, it is important to define the scope of the work required in the letter of engagement, in order to be clear on the costs to be incurred and to specify what the deliverable will be – i.e. a summary “exceptions based” report, or a detailed document covering every aspect of the Target. A summary exceptions based report is usually advisable since it focuses on any key risks identified and is more reader-friendly.

When asking external advisors for engagement proposals it is important to provide as much detail as possible to those you are putting the due diligence engagement out to tender with (of course, being mindful of any confidentiality issues) in order for the advisors to put together a realistic and comprehensive quote. Any time sensitivities should also be communicated so these can be accounted for in proposals.

If possible, request a comprehensive service package (often covering financial, tax, legal, HR) since it is much easier to deal with one external advisor. In addition to using a single advisor, it is also common to appoint external advisors to cover the areas of financial and legal due diligence and to cover commercial, HR and operational due diligence in-house.

If working with external advisors it is important to ask for details of past deals/projects the advisors have worked on (ideally in the in the same sector as the Target). A strong understanding of the sector in which the Target is based will maximise the chance of the advisor(s) spotting key issues, price reducers or potential deal breakers.

Preparation

As early as practically possible the acquirer should form and begin briefing the due diligence team. A team should consist of skilled financial and legal advisors (all preferably with M&A experience – ideally in the sector of the Target but not essential) as well as being subject matter experts in all key areas falling within the scope of the due diligence engagement.

- External advisors should be considered if the acquirer lacks any of the required expertise necessary for a successful transaction – for instance, lawyers, accountants, consultants and/or investment-bank.

- Due diligence checklists should be drafted to cover the areas in scope (typically financial, commercial, operational, legal, human resources and other such as regulatory and environmental).

- Data requests should be prepared and shared with the Target (and their advisors) once the scope of the due diligence engagement and price has been agreed.

- The acquirer should negotiate and sign a confidentiality agreement/non disclosure agreement (NDA). This is typically issued by the Target and facilitates the exchange of sensitive information while restricting the acquirer from sharing information with third parties.

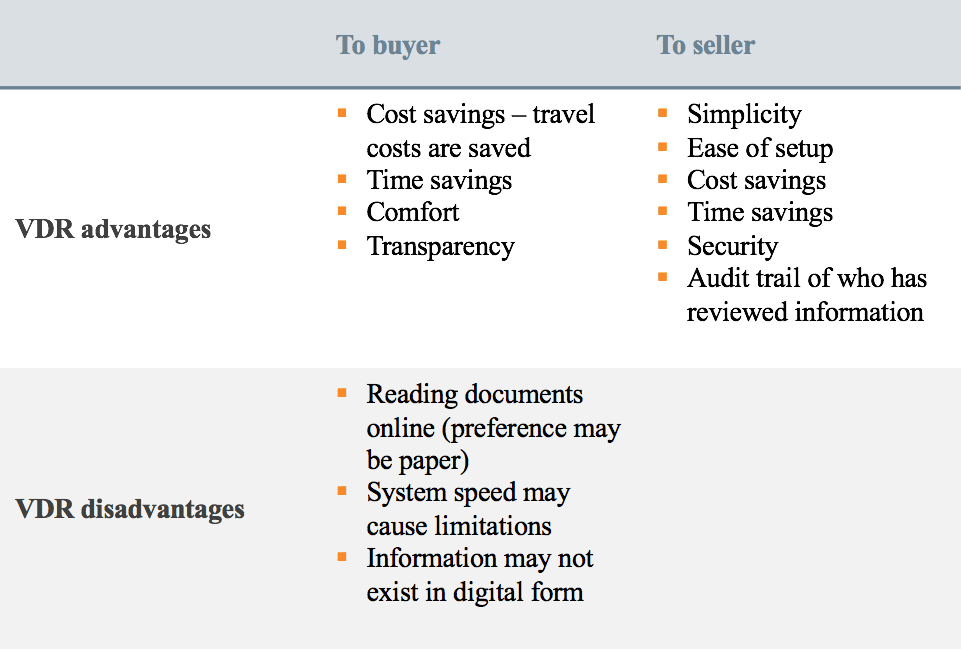

- Consideration should be given to establishing a physical or virtual (online) data room for the collating of confidential documents (a virtual data room is cheaper and more efficient, accessible via secure log-in and depending on the data room chosen allows for users to be provided with differing access rights).

Working with Virtual Data Rooms (VDRs)

A virtual data room (VDR) is an online store of information used for the collating and distribution of key documents in the due diligence process. Physical data rooms (PDRs) have traditionally been used – however, for reasons of cost, efficiency, logistics and security, virtual data rooms have widely replaced physical data rooms.

Benefits of a Virtual Data Room

- Added Security — documents are usually kept in audited data-centres and encrypted during both storage and transfer phases;

- Detailed Reporting — both the Target and acquirer may receive email alerts about file activity and follow detailed audit reports back to the source;

- Advanced Tools — VDRs often allow users to drag and drop files and sync account folders;

- Ease of Use — there is no training necessary, and the cloud-based format means you have no additional hardware requirements.

A growing number of companies looking to acquire have modernized the way they exchange information as part of their due diligence process. Rather than sending their due diligence questionnaires to the Target and relying on the Target’s provided virtual data room, the acquirers themselves can now invite the Target to their own buy-side platform to answer those questions and provide the necessary documents.

Buy-side due diligence software, a form of reverse-VDR, can significantly reduce the buy-side team’s workload and provide them with right material in real-time.

The Due Diligence Process

The due diligence team will be working to confirm the Target’s representations, validate the valuation agreed in the LOI, investigate any legal, regulatory and compliance concerns, and confirm anticipated synergies and post-merger integration steps.

It is also necessary for the team to consider the “soft” aspects of the Target, such as its corporate culture so as to assess its fit with any of the acquirer’s existing group companies. Key questions the due diligence team should be mindful of include:

- Are there any problems with the Target, which would force you to abandon the deal, even given a significant price reduction?;

- Are there any issues that should bring about a change in the structure, terms, or price of the transaction?;

- Do the Target’s financial statements accurately reflect the company’s financial position?;

- Would the integration of existing operations with those of the Target have any adverse effect on profitability?;

- What is the Target’s outlook in terms of its customer base and concentration, its competitive positioning, and its ability to preserve or increase its profit margins?;

- Is the Target exposed to any significant and unexpected regulatory, governance, or liability risks?;

- Have future costs (for instance – a pension deficit) been figured into the acquisition value?;

- What is the composition and expertise of the Target’s key management team?

Due Diligence Etiquette – Key Considerations

- The amount of interaction with the Target – in particular, key management and employees;

- The role of external advisors (lawyers, accountants, corporate finance, consultants, investment banks);

- The expertise and availability of internal resources (such as legal and tax advisors);

- How much time is available for the due diligence engagement and whether either side has set a deadline for the transaction to complete by;

- Request periodic reporting of findings during the process – deal breakers must be highlighted immediately as they are being discovered so that the appropriate remedying action can be taken;

- Schedule regular catch up meetings/conference calls so that all advisors are on the “same page”.

Common DD Mistakes

- The due diligence team may misidentify the risks associated with the acquisition or may become so focused on their individual functions that they miss the “big picture”;

- The team may overlook the “soft” but important elements of the Target’s corporate culture;

- The team may disclose anticipated synergies associated with the Target to the Target (leading the Target to increase their asking price to capture this value, for instance);

- The team may rely solely on virtual due diligence and never conduct on-site fieldwork.

Key Takeaways

- Understand exactly what you are acquiring;

- Valuations need to be underpinned by effective due diligence;

- Consider “deal-breakers” or “deal-amenders” – look for problems with the Target that are fundamental deal-breakers, forcing you to abandon the transaction. Similarly, look for issues that can bring about changes in the structure, terms, or price of the transaction;

- Give due attention to the retention of key staff;

- If the due diligence team uncovers problems be prepared to walk away from the transaction.